Halaman yang Anda Cari Tidak Tersedia

Halaman yang Anda Cari Tidak Tersedia

In contrast to its threatened 25% tariffs on exports from Canada and Mexico, America’s additional 10% tariffs on Chinese exports came into force yesterday.

Source: Bank of Singapore, Bloomberg

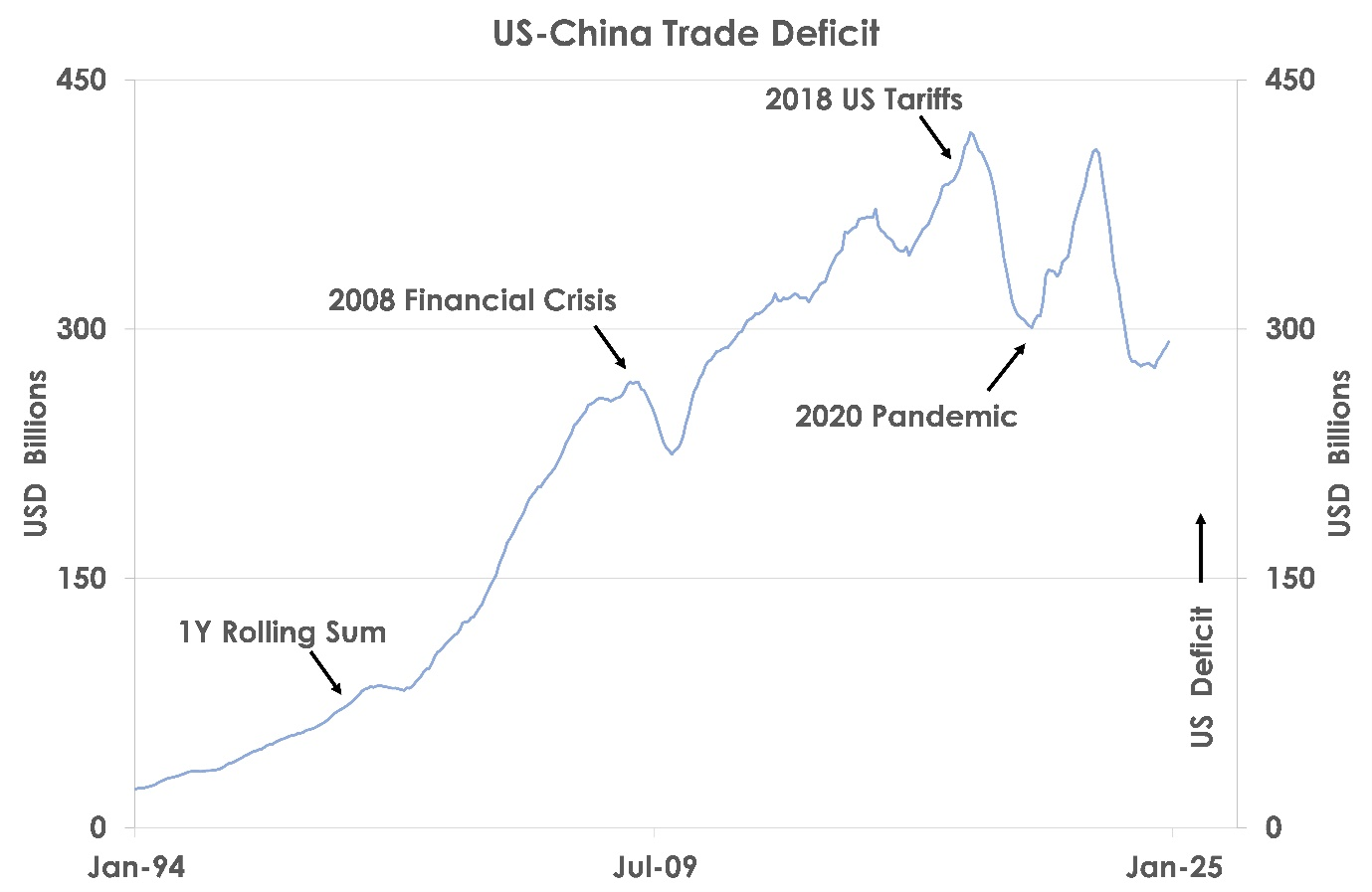

In 2024, China’s exports to the US were USD525bn as shown in the chart or almost 3% of China’s GDP. But, overnight, investor reaction was muted as Beijing’s response was limited to four targeted actions.

Firstly, retaliatory tariffs were only imposed on select US exports to China amounting to just USD14 billion last year. 10% tariffs were set on US crude oil, agricultural machinery and vehicles and 15% tariffs on US exports of coal and liquid natural gas (LNG).

Secondly, two US firms were added to China’s ‘unreliable entity list’, restricting their activities.

Source: Bank of Singapore, Bloomberg

Thirdly, investigations were announced into three US tech firms and, fourth, export bans were imposed on five critical minerals including tungsten where China is the world’s dominant producer.

China’s response leaves the door open for a potential deal between Washington and Beijing to avert a more damaging, broader trade war. Its new restrictions also will not take effect until February 10.

Investors may also have been relieved that the US levies on Chinese exports were not higher. President Trump had proposed tariffs as high as 60% before his second term began. But if the US keeps additional tariffs on all Chinese exports at 10%, the impact on China’s 2025 GDP growth should be manageable.

The second chart shows when the first Trump administration set 10-25% tariffs on USD200 billion of Chinese exports in 2018, China’s trade surplus with the US fell from over USD400 billion to USD300 billion though Beijing also agreed to buy more US goods.

Similarly, in 2025, America’s broad 10% tariffs may shave USD100 billion or around 0.5% off China’s GDP, reducing growth from 5.0% in 2024 to 4.5% this year. But if US tariffs are set at 20-30% then China’s growth may fall more sharply towards 4.0% in 2025.

US-China talks will thus be key for limiting downside risks to Chinese markets and the CNY. If negotiations are fruitless and US tariffs increase further, then financial markets will react more strongly this year.

This article was first published by Bank of Singapore on 5 February, 2025. The Opinions expressed in this publication are those of the authors. They do not purport to reflect the opinions or views of OCBC Private Bank or its affiliates.

OCBC Private Bank provides a suite of products for wealth creation, preservation and transmission including holistic wealth management services, independent research, customized solutions for all investor preferences, and genuine open architecture, with expertise in Indonesia and Asia Pacific markets. OCBC Private Bank is a part of OCBC Group.